From Knowledge@Wharton:

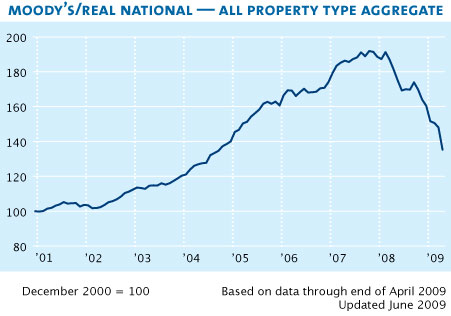

"The shoe has already dropped," says Wharton real estate professor Susan Wachter. "Values are down severely. Vacancy rates are at 20-year highs." The Federal Reserve reports that delinquency rates on commercial real estate loans have doubled in the past year to 7%, as companies pull back on commercial space and retailers go out of business.

Typically, commercial real estate developers help lead the nation from boom into bust by constructing too much space and defaulting on loans, jeopardizing the stability of lending institutions. This time, problems in the financial sector are branching out into commercial property.

"This is entirely a financial crisis, first and foremost. The problem is the seizing up of financial markets, not overbuilding as in the past," Wachter says. "The overall economy is weak and weakening, which is driving down rents. Past real estate crises were centered in real estate without an economy-wide crisis at the same time."

With financing tight, it is difficult or impossible for property owners to rollover short-term financing when it comes due. For example, General Growth Properties, the second-largest shopping mall company, filed for bankruptcy court protection after its lenders refused to refinance $27 billion in debt. The Real Estate Roundtable in Washington, D.C., estimates $400 billion in commercial real estate loans will come due this year. By 2012, the figure will be more than $1.8 trillion.

Wachter sees a bifurcation in the commercial real estate sector. Large, publicly traded real estate investment trusts (REITs), with equity in projects and access to public markets, are best positioned to ride out the downturn, she says. Other real estate firms, particularly those controlled by private equity funds that face short-term debt obligations to financial institutions that are in trouble themselves, will have less flexibility.

An Opportunity?

"This is an opportunity -- or may be an opportunity soon -- for REITs that are positioning themselves to take advantage of other companies and bottom fish to purchase significant properties at bargain basement prices," says Wachter. She cites plans by Vornado Realty Trust to raise $1 billion to create a fund to invest in distressed properties. "It's back to 'cash is everything.'"

Indeed, publicly held REITs reported strong second-quarter results. The Dow Jones Equity All REIT Total Return Index, composed of 114 REIT stocks, rose 28.9% -- the largest increase since the index was created in 1989.

Brian Case, vice president of research for the National Association of Real Estate Investment Trusts, says many REITs have shored up their positions with cash raised in secondary offerings. In the future, he expects to see a new wave of initial public offerings (IPOs) by private real estate investors who are proven managers with strong portfolios, but who are also under pressure from debt that is coming due. In a better credit environment, that debt might have easily rolled over, but in the current climate an IPO may be the only source of new money. They have two choices: sell into a very soft market through 2012 or, if they are strong enough, do an IPO and use that equity to meet debt obligations," according to Case.

Meanwhile, the U.S. government is attempting to ease the crisis by extending its Term-Asset-Backed Securities Loan Facility (TALF) to troubled commercial real estate firms. The program opened for new real estate loans earlier this summer but received little interest. The TALF program was then extended to existing commercial mortgage securities. On July 16, the Federal Reserve Bank of New York said investors sought $668.9 million worth of loans to buy securities backed by commercial real estate loans that were made months or years ago. Two days earlier, Standard & Poor's cut ratings on commercial real estate bonds issued by Goldman Sachs, JPMorgan Chase and other financial institutions, effectively disqualifying billions in bad loans from the government program.

"The government has successfully stopped runs on banks and has stabilized the banking economy, but that doesn't mean it can coerce banks to make loans to entities where the value of their collateral is down as much as in real estate," says Wachter.

Total losses in securities backed by commercial property loans could climb as high as $90 billion in the next few years, according to Deutsche Bank analyst Richard Parkus, who also testified during the recent Joint Economic Committee hearings. In addition, he estimated up to $140 billion in losses from construction loans made by regional and local banks is also in jeopardy. "We believe the bottom is several years away," Parkus told the committee.

Wachter says the use of commercial mortgage-backed securities (CMBS) was not as flawed as mortgage-backed securitization in residential markets, but she predicts the CMBS market will face reforms before it becomes a force in commercial real estate finance again. Ultimately, however, securitization will continue to be an important element in structuring commercial real estate finance. "How it comes back is still in question, but it will come back. There are some clear issues with CMBS."

In the meantime, property owners are scrambling to renegotiate with tenants and reposition properties to make them more likely to receive continued financing. Wharton marketing professor Stephen J. Hoch says retailers are approaching landlords and threatening to close their doors if they don't receive concessions. "The REITs have adapted and tried to be proactive," says Hoch. "It's taken a catastrophe to wake up and smell the coffee."