CRE & Capital Markets - Implications for California

From the California State Controller's Office, November 2009 Economic Summary Analysis:

Capital Markets and Valuation

Whereas excessive and imprudent leverage fed the bubble, deleveraging not only popped the bubble, but, in the process, destroyed record amounts of equity and debt. Most deals financed with high leverage from 2005 to the present are under water. The equity is gone and the debt, if it trades at all, trades at a deep discount to face value. Most leveraged equity invested in real estate has evaporated since property prices, if marked to market, have fallen 30% to 50%.

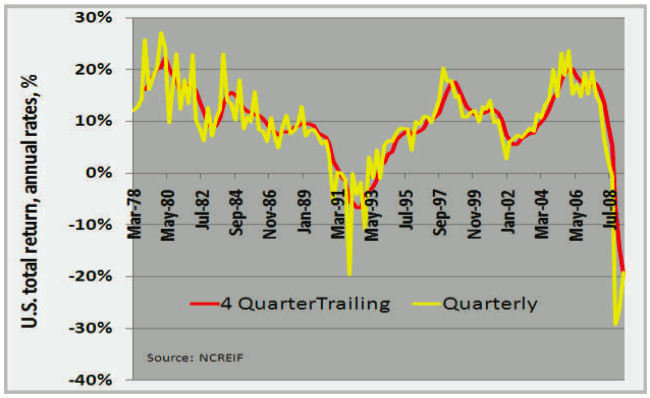

The chart above shows overall U.S. property total returns, quarterly (at annual rates) and lagging four quarters. This appraisal-based, lagging index shows sharp negative returns exceeding the deterioration of the RTC (Resolution Trust Corp.) period of the early 1990s. Second quarter 2009 returns indicate the possibility that total returns, while still negative, may have hit a point of inflection. We expect that property values in many sectors, especially office, retail, and industrial, will likely deteriorate further in 2010 with improvement beginning sometime in 2011.

The deflationary spiral is ongoing and likely to proceed much further. The economy is deleveraging, a painful process that spares few sectors, least of all real estate. At present there is a historic capital markets imbalance, the resolution of which awaits the massive in-process repricing of all commercial real estate. We believe that, despite the availability of few sales comparables, the bottom of the cycle is at hand.

The inability of many banks and other capital sources to lend not just to real estate firms but to other businesses in the State as well presents a real challenge to the private sector and state

and local governments.

Property—National and California Perspectives

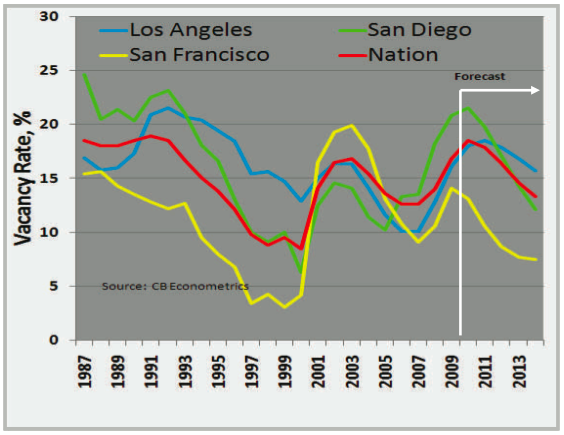

Commercial property operations — occupancy and rental growth — remain weak. The good news is that vacancy rates are peaking in most commercial property categories in California and elsewhere across the nation. The recent trend and outlook for vacancy rates in Los Angeles, San Diego, and San Francisco mirror the nation, as shown in the chart above.

Implications for California

The economic crash and its aftermath are affecting all sectors of the economy, real estate being no exception. Real estate, especially in the transactional sub-sectors (e.g., brokers, etc.), accounts for a significant share of the California labor force. The downturn has created a vicious negative feedback, a symptom of which is still ongoing property deflation and tenant defaults. Attendant symptoms are reduced property tax revenues, failing businesses, decimated transactions volume, and reduced income and sales tax revenues. The extent to which the recovery is delayed will depend on a number of factors, not least of which is the extent and timing of loss recognition by owners and financial institutions.

Capital Markets and Valuation

Whereas excessive and imprudent leverage fed the bubble, deleveraging not only popped the bubble, but, in the process, destroyed record amounts of equity and debt. Most deals financed with high leverage from 2005 to the present are under water. The equity is gone and the debt, if it trades at all, trades at a deep discount to face value. Most leveraged equity invested in real estate has evaporated since property prices, if marked to market, have fallen 30% to 50%.

The chart above shows overall U.S. property total returns, quarterly (at annual rates) and lagging four quarters. This appraisal-based, lagging index shows sharp negative returns exceeding the deterioration of the RTC (Resolution Trust Corp.) period of the early 1990s. Second quarter 2009 returns indicate the possibility that total returns, while still negative, may have hit a point of inflection. We expect that property values in many sectors, especially office, retail, and industrial, will likely deteriorate further in 2010 with improvement beginning sometime in 2011.

The deflationary spiral is ongoing and likely to proceed much further. The economy is deleveraging, a painful process that spares few sectors, least of all real estate. At present there is a historic capital markets imbalance, the resolution of which awaits the massive in-process repricing of all commercial real estate. We believe that, despite the availability of few sales comparables, the bottom of the cycle is at hand.

Emphasis added by ENSO: Highlighted text seems to be somewhat contradictory and typical of ungrounded optimism endemic in certain quarters of the financial markets.A crisis of unprecedented proportions is approaching. Of the $3 trillion of outstanding mortgage debt, $1.4 trillion is scheduled to mature in four years. We estimate another $500 billion to $750 billion of unscheduled maturities (i.e., defaults). Unfortunately, traditional lenders of consequence are practically out of the market and massive amounts of maturing debt will not easily find refinancing. Marking-to-market outstanding debt will render many banks, especially regional and community banks, insolvent, especially as much of the debt is likely worth about 50% of par, or less.

The inability of many banks and other capital sources to lend not just to real estate firms but to other businesses in the State as well presents a real challenge to the private sector and state

and local governments.

Property—National and California Perspectives

Commercial property operations — occupancy and rental growth — remain weak. The good news is that vacancy rates are peaking in most commercial property categories in California and elsewhere across the nation. The recent trend and outlook for vacancy rates in Los Angeles, San Diego, and San Francisco mirror the nation, as shown in the chart above.

Emphasis added by ENSO: A "peak" in vacancy rates can only be determined a posterioriSan Francisco, of the three profiled California cities, has the lowest vacancy rate. Since the city’s vacancy rate will reach equilibrium sooner, rental growth will turn positive as early as 2010. However, Los Angeles and San Diego will likely lag by as much as two years.

Implications for California

The economic crash and its aftermath are affecting all sectors of the economy, real estate being no exception. Real estate, especially in the transactional sub-sectors (e.g., brokers, etc.), accounts for a significant share of the California labor force. The downturn has created a vicious negative feedback, a symptom of which is still ongoing property deflation and tenant defaults. Attendant symptoms are reduced property tax revenues, failing businesses, decimated transactions volume, and reduced income and sales tax revenues. The extent to which the recovery is delayed will depend on a number of factors, not least of which is the extent and timing of loss recognition by owners and financial institutions.

posted by ENSO Advisors at

8:10 AM

![]()

<< Home