Classic Jon Stewart....

Record Level Enforcement Actions in 2009

Excerpts from American Banker: Regulatory Actions Hit a Record Level in '09: "Bank regulators issued 1,143 formal enforcement actions against banks and their holding companies last year, a new record and more than double the 2008 tally." "Informal actions by the agencies, which are not made public and often go untracked, also doubled during that time, reaching 1,099 last year, according to data provided to American Banker." According to the FDIC quarterly banking profile, there were 8,012 insured banks at the end of 2009. Some of these actions are double counts since regulators might issue a Memorandum Of Understanding and then a formal Cease & Desist action against the same bank (or multiple formal actions), so the exact percentage of banks operating under enforcement actions (either formal or informal) can't be determined, but it could be in the 20% to 25% range.

How to Buy a Toxic Asset

Get the details of their experiment and track their results here

More Pain for Banks

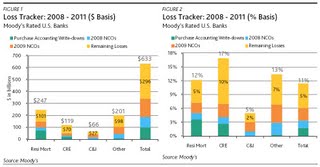

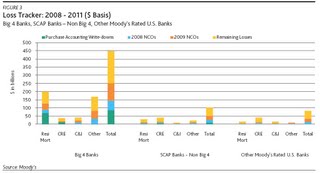

A new report by Moody's "U.S. Bank Asset Quality: Negative Trends Slow Down, But The Pain Isn't Over" has some gloomy observations about the asset quality of the US financial system, and its implications for future charge offs and overall profitability. In estimating total loan charge-offs between 2008 and 2011 Moody's predicts that of the total $536 billion (really $633 billion if unadjusted for purchasing accounting marks), which is equal to 9.7% of all loan outstanding at December 31, 2007, only $240 billion has been charged off, leaving $296 billion still to hit the books. Yet banks have taken loan loss allowances of "only" $188 billion, leaving just over $100 billion unaccounted for. And people wonder why banks are unwilling to lend. Moody's conclusion on what happens as reality catches up with charge offs: "Although banks have provisioned for a substantial amount of their remaining charge-offs, the additional provision required will extend the period that many banks will be unprofitable well into 2010, and will reduce capital levels." Obviously, Moody's estimates do not go past 2011 when many anticipate the next major wave of loan impairments to occur in the form of Option ARM resets and Commercial Real Estate maturities. Furthermore, Moody's does not account for securitized credit card losses, which will also be an area of major pain for the banks in the upcoming years. Just how big the impact of all these will be is still to be determined although it is very likely that the overall impact will impair overall bank capital by well over $100 billion over the next several years. From the Moody's report: Moody’s estimates that rated U.S. banks will incur $536 billion of loan losses between 2008 and 2011, equal to 9.7% of loans outstanding at December 31, 2007. We have incorporated this amount into our views of banks’ capital adequacy and into our ratings. This amount has been reduced for the purchase accounting marks taken on residential and commercial mortgage portfolios in recent acquisitions, including JP Morgan’s purchase of Washington Mutual, Wells Fargo’s purchase of Wachovia, Bank of America’s purchases of Countrywide and Merrill Lynch, and PNC’s purchase of National City. On a gross basis (prior to the reduction by the purchase accounting marks), Moody’s loss estimate is $633 billion, or 11.4% of loans outstanding at December 31, 2007. Essentially, we believe charge-offs equal to 1.7% of loans were eliminated through purchase accounting write-downs. Note that these estimates exclude securitized credit cards. The charts and table below summarize our gross loss estimates in dollar and percentage terms by asset class for all rated U.S. banks (Figures 1 and 2). Each asset class is broken down as follows: charge-offs that have been eliminated through purchase accounting write-downs, 2008 charge-offs, 2009 charge-offs, and the remaining losses that would need to be incurred to reach our full estimate. Rated U.S. banks charged off $88 billion of loans in 2008 and $152 billion in 2009, leaving $296 billion, or 5.3% of loans, to be charged off in 2010 and 2011 to reach our full estimate. Therefore, rated U.S. banks have recognized 45% of our anticipated net charge-offs. On an asset class basis, we believe 42% of residential mortgage losses have been taken versus 30% for CRE.  And despite some minor good news in the trend, the overall pattern is still one which should force financial analysts to reevaluate their Strong Buy ratings on most banks: Although the increase in charge-offs between 2008 and 2009 is substantial, the quarterly charge-off trend moderated at the end of 2009 with aggregate charge-offs actually declining slightly (from $41.3 billion to $40.2 billion) between the third and fourth quarters of 2009. This slow down in net charge-off recognition for rated U.S. banks did not change our forecast of the amount of charge-offs rated U.S. banks will incur, but it has changed our expectations regarding the timing of when these losses will be recognized. Previously, we had anticipated that rated U.S. banks would incur elevated charge-offs through 2010 and return to a more normalized level of charge-offs in 2011. However, we now anticipate that banks will still be grappling with elevated charge-offs through at least the first half of 2011. The TBTF Big 4 (BofA, Wells, JPM and Citi) comprise the bulk of the charge off risk. The Big have merely gotten Bigger, and now represent an even more concetrated threat to the US economy once true marks are let out of the bag. Figure 3 summarizes our gross loss estimate in dollar terms for the following bank groups: “Big 4 Banks”, “SCAP Banks – Non Big ”, and “Other Moody’s Rated U.S. Banks” . Our gross loss estimates for the Big 4 Banks, SCAP Banks – Non Big 4, and Other Moody’s Rated U.S. Banks are $447 billion (12.9%), $104 billion (10.4%), and $81 billion (7.5%), respectively. In comparison to our estimate that rated U.S. banks are 45% of the way through their net charge-offs, we believe the Big 4 Banks are 46% of the way through their net charge-offs, while SCAP Banks – Non Big 4 and Other Moody’s Rated U.S. Banks are each 43%.  And here is how many remaining losses at all banks and the Big 4 will still need to be digested.  Full report here.

Another Record In CMBS Delinquencies

The announcement by Fitch that CMBS delinquencies rose by another 29 bps to a new high of 6.29% is no surprise to anyone who has been following RealPoint's remittance/CMBS reports. Yet it is good to get independent confirmation that there is no respite in CMBS land. And with TALF for existing and new loans expiring on March 31 and June 31 respectively, without ever really taking of, this sector of the market is sure to face increasing pressure, especially when coupled with the certain increase in MBS rates once the last $30 billion or so in QE is purchased. The most recent culprit for deterioration: maturities of 5 year loans from the 2005 vintage as the refi market is still practically dead: "Approximately 30% of the newly delinquent loans were from 2005 transactions. In fact, the four largest newly delinquent loans (ranging in size from $65 million to $112 million) are from this vintage. Three of these four loans are past their 2010 maturity dates and are, therefore, categorized as non-performing matured loans." Full Fitch report: Fitch Ratings-New York-08 March 2010: Upcoming maturities from U.S. CMBS deals originated in 2005 contributed to a 29 basis-point (bp) increase in delinquencies to 6.29% at the end of February, according to the latest U.S. CMBS delinquency index results from Fitch Ratings. Approximately 30% of the newly delinquent loans were from 2005 transactions. In fact, the four largest newly delinquent loans (ranging in size from $65 million to $112 million) are from this vintage. Three of these four loans are past their 2010 maturity dates and are, therefore, categorized as non-performing matured loans. "Five-year loans originated in 2005 will continue to have difficulty refinancing this year as liquidity remains limited,' according to Managing Director Mary MacNeill. 'In many cases, sponsors will have to either contribute additional equity in order to refinance their loans or look to the servicers for extensions and modifications." For the first time, office properties saw a greater than overall average increase in the index, with a 45 bp movement month over month in comparison to the overall index of 29 bps as three of the top four newly delinquent loans are office properties. Multifamily and industrial also exceeded the overall index change at 64 and 43 bps respectively. When the Peter Cooper Village/Stuyvesant Town loan hits 60 days delinquent, the overall index will increase 60 bps and multifamily will increase by over 400 bps. Current delinquency rates by property type are as follows: Office: 3.50%; Hotel: 16.61%; Retail: 5.09%; Multifamily: 8.97%; Industrial: 4.16%. Fitch's delinquency index includes 2,505 loans totaling $28.5 billion of the Fitch rated universe of approximately 42,000 loans comprising $452.6 billion that are at least 60 days delinquent or in foreclosure. The Index excludes Fitch-rated loans that are 30 to 59 days delinquent, which currently total $3.2 billion.

‘On the Edge’ Banks Facing Writedowns After FDIC Loan Auctions

A Federal Deposit Insurance Corp. plan to auction more than $1 billion in assets seized from failed banks next month, including a loan to build a , may trigger write downs that weaken lenders nationwide. Almost half of the loans were originated by Silverton Bank N.A., whose collapse last May was the biggest in Georgia history. Community banks that joined Silverton in providing $80 million for the 237-room W Hotel and condominium complex in Atlanta, as well as backing for 39 other projects, could be forced to write down their stakes to reflect sale prices. The auctions may have wider repercussions. Of the $50.4 billion in loans seized from failed banks currently held by the FDIC, 63% involve participations by other lenders, according to data provided by agency spokesman Greg Hernandez. “These banks can’t believe that the regulator they pay to protect them is going to sell these loans to someone who can flip them and cause them serious losses,” said Robert Reynolds, a lawyer at Reynolds Reynolds & Duncan LLC in Tuscaloosa, Alabama, who represents 25 lenders that took part in financing the W Hotel. “Our banks just cannot believe they’re being treated in a way that ultimately hurts the FDIC’s insurance fund, because some of them are right on the edge.” Bank FailuresA total of 140 banks failed last year, and FDIC Chairman Sheila Bair said the number may be higher this year. It stands at 26 as of March 6. The agency said on Feb. 23 that 702 banks were on its “problem” list as of Dec. 31, up from 552 at the end of the third quarter. The FDIC’s insurance fund had a deficit of $20.9 billion at the end of the year. “This whole thing is a mess waiting to happen across the country,” said Geoffrey Miller, a professor of securities law at New York University and director of the Center for the Study of Central Banks and Financial Institutions. “Unlike the subprime mortgage problems, which hit mostly bigger financial institutions, the commercial real estate crisis is going to hit mostly smaller and regional banks,” Miller said. “It was common for them to make these loans and buy participations. It’s a systemic problem that the FDIC has to deal with.” That view was echoed by John J. Collins, president of Community Bankers of Washington in Lakewood, Washington. Some banks in his state have expressed concern that they may have to take write downs as a result of the FDIC sale of seized loans in which they participated, he said. “We have a number of banks teetering on the edge, and we don’t need this problem,” Collins said in an interview. ‘Decreases’ ValueIf a loan is sold to a buyer who restructures it at less than book value or forecloses on the property, participating banks would have to write down their stakes, said Russell Mallett, a partner at PricewaterhouseCoopers LLP in New York who specializes in bank accounting. Absent a restructuring, banks have flexibility in how they value loans, he said. “This is not a perfect real estate development, but it could work its way out of its problems if they get more funding and we’re patient,” said Ralph Banks, executive vice president of Merchants & Farmers Bank of Greene County in Eutaw, Alabama, which owns less than $1 million of the loan. That view was supported by executives at two other lenders that bought participations who asked not to be identified because their banks’ roles as owners of the W Hotel loan haven’t been disclosed. The FDIC has a policy of not splitting servicing rights from loan ownership because it “decreases the value of those assets,” said Hernandez, the agency spokesman. ‘Deal With Themselves’Reynolds said the banks he represents may bid for Silverton’s share of the W Hotel loan if they can come up with the capital in order to stave off write downs. Some of the lenders are already in financial trouble, he said, declining to identify them. One that participated in the loan, Florida Community Bank in Immokalee, Florida, failed on Jan. 29. Silverton, a wholesale bank based in Atlanta with no consumer operations, was owned and overseen by more than 400 community lenders in the region. It was founded in 1986 and provided banking services, including wire-transfer systems, bond trading and credit-card operations, to about 1,400 institutions in 44 states. Reynolds said the banks that owned Silverton, some of which had representatives on its board, never imagined it would fail. “My clients had a long, successful record with Silverton,” Reynolds said. “When they signed their participations, they felt they were signing a deal with themselves because they all owned the bank. We all thought this was a way to diversify risk.” Silverton FailureThe bank’s troubles began in early 2007, when it changed from a state to a national charter so it could accelerate its growth, according to a report by the Treasury Department’s Office of Inspector General, which reviews failures of banks regulated by the Office of the Comptroller of the Currency. Silverton’s commercial real estate lending rose to $1.2 billion at the end of 2008 from $681 million at the end of 2006, the report said. The bank had $4.1 billion in assets when it failed last year, and the FDIC said the closing will cost its insurance fund $1.3 billion. “The board and management either chose to ignore or failed to acknowledge the indicators of a declining real estate market,” the inspector general’s report said. Defaults DoubleReal estate loans at U.S. banks that are at least 90 days overdue or that are expected to default almost doubled in 12 months to 7.1 percent, according to December FDIC data. Non- performing loans for construction and development rose to 16 percent from 8.6 percent. “This is a situation the FDIC is going to face more, since the number of bank failures is going up,” said Gerard Cassidy, an analyst at RBC Capital Markets in Portland, Maine. “The FDIC is not in the business of managing loans, so they do have to sell them. But they also have to look at the bigger picture and take a global approach by liquidating those assets without hurting the banks that bought participations.”

Advice for Obama: A Presidential Reunion

CMBS Delinquencies Hit Record At $46 Billion

On one hand you have Moody's REAL CPPI index telling you commercial real estate prices not only bottomed in December, but are now increasing at the fastest rate in years. On the other hand you have reality staring you in the face (that is if you are reading the February RealPoint CMBS report), in the form of $46 billion in CMBS delinquencies in January: this was a record 5.762% of total, and represents a 325% increase from the $10.8 billion in January 2009 (and a 10% increase sequentially). Contrary to all propaganda punditry, the rate of deterioration in commercial real estate keeps accelerating. Oh, and this number does not include the $3 billion Stuy Town default, which will be counted for the first time in March. Look for the % of delinquent loans to hit 8%-9% within 6 months, about the time when TALF will be really needed. Too bad TALF expires the same day as Quantitative Easing for MBS ends, March 31.  More from Realpoint: Overall, the total unpaid balance for CMBS pools reviewed by Realpoint for the January 2010 remittance was $797.3 billion, up slightly from $797.18 billion in December 2009 (affected by some servicer and trustee reporting delays). Both the delinquent unpaid balance and delinquency percentage over the trailing twelve months are shown in Charts 1 and 2, clearly trending upward. The resultant delinquency ratio for January 2010 of 5.76% (up from the 5.22% reported one month prior) is over four times the 1.281% reported one-year prior in January 2009 and 20 times the Realpoint recorded low point of 0.283% from June 2007. The increase in both delinquent unpaid balance and ratio over this time horizon reflects a steady increase from historic lows in mid-2007. The $4.1 billion Extended Stay Hotel loan from the WBC07ESH transaction remained 90+-days delinquent in January 2010. Realpoint expects the delinquency for this loan to continue in the near-term until any modification or restructuring agreement is reached. In addition, the $3 billion Peter Cooper Village / Stuyvesant Town loan spread through multiple CMBS deals via pari passu structure is now expected to be reported delinquent in March 2010. On January 25, 2010, Tishman Speyer announced their intention to transfer title to the Lender via Deed-in-Lieu of foreclosure. The Borrower initially sought a forbearance (which was not granted), and ultimately did not make the full payment due in January 2010, which triggered a default under the mortgage loan. Funds have subsequently been swept from all reserves / escrows and applied to debt service in January and February 2010 (thus reserves are essentially depleted) and the borrower has indicated it will no longer fund debt service shortfalls. Therefore, with the $4.1 billion delinquency of the Extended Stay Hotel loan, the expected delinquency of the $3 billion Peter Cooper Village / Stuyvesant Town loan, and the experienced average growth monthover-month, Realpoint now projects the delinquent unpaid CMBS balance to continue along its current trend and grow to between $60 and $70 billion by mid 2010. Based upon an updated trend analysis, we now project the delinquency percentage to grow to between 6% and 7% through the first quarter of 2010, potentially approaching and surpassing 8-9% under more heavily stressed scenarios through the mid-2010). This forecast / outlook is driven by the watchlist reporting of several Realpoint identified High Risk Loans from recent vintage transactions that continue to show signs of stress and are on the verge of delinquency, along with continued balloon maturity defaults from more seasoned transactions. As part of our monthly surveillance efforts of every CMBS transaction, we continue to monitor in detail many large Realpoint Watchlisted loans that have never met their pro-forma underwritten expectations. This includes a large amount of loans that remain current in payments but have already been transferred into special servicing - many of which may ultimately default based upon a denial of requests for loan modifications or debt restructuring by the special servicers, or a decision by borrowers to surrender the collateral. With TALF expiring soon, is it time to start, if not panicking, then realizing that mere good intentions and a large vocabulary will not do much for the billions in missing interest expense that will result in creeping defaults across all CMBS classes and vintages. For those who still believe glimmers of reality may eventually creep into capital markets, here are RealPoint's near-term projections. Over the past three months, delinquency growth by unpaid balance has averaged roughly $4.47 billion per month. Assuming ongoing monthly pay-down and liquidation activity, if such delinquency average were increased by an additional 25% growth rate, and then carried through the first quarter 2010, the delinquent unpaid balance would reach $57 billion and reflect a delinquency percentage slightly above 7% by March 2010. Carried through mid-2010, the delinquent unpaid balance would top $73 billion and reflect a delinquency percentage above 9.5% by June 2010. In addition to this growth scenario, if we again add-in the default of the $3 billion Peter Cooper Village / Stuyvesant Town loan, the delinquent unpaid balance would reach $60 billion and reflect a delinquency percentage above 7.6% by March 2010. Carried through mid-2010, the delinquent unpaid balance would top $76.9 billion and reflect a delinquency percentage near 10% by June 2010. Source: Zero Hedge

|