More Pain for Banks

A new report by Moody's "U.S. Bank Asset Quality: Negative Trends Slow Down, But The Pain Isn't Over" has some gloomy observations about the asset quality of the US financial system, and its implications for future charge offs and overall profitability. In estimating total loan charge-offs between 2008 and 2011 Moody's predicts that of the total $536 billion (really $633 billion if unadjusted for purchasing accounting marks), which is equal to 9.7% of all loan outstanding at December 31, 2007, only $240 billion has been charged off, leaving $296 billion still to hit the books. Yet banks have taken loan loss allowances of "only" $188 billion, leaving just over $100 billion unaccounted for. And people wonder why banks are unwilling to lend. Moody's conclusion on what happens as reality catches up with charge offs: "Although banks have provisioned for a substantial amount of their remaining charge-offs, the additional provision required will extend the period that many banks will be unprofitable well into 2010, and will reduce capital levels." Obviously, Moody's estimates do not go past 2011 when many anticipate the next major wave of loan impairments to occur in the form of Option ARM resets and Commercial Real Estate maturities. Furthermore, Moody's does not account for securitized credit card losses, which will also be an area of major pain for the banks in the upcoming years. Just how big the impact of all these will be is still to be determined although it is very likely that the overall impact will impair overall bank capital by well over $100 billion over the next several years.

From the Moody's report:

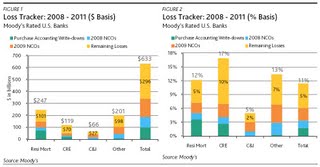

Moody’s estimates that rated U.S. banks will incur $536 billion of loan losses between 2008 and 2011, equal to 9.7% of loans outstanding at December 31, 2007. We have incorporated this amount into our views of banks’ capital adequacy and into our ratings. This amount has been reduced for the purchase accounting marks taken on residential and commercial mortgage portfolios in recent acquisitions, including JP Morgan’s purchase of Washington Mutual, Wells Fargo’s purchase of Wachovia, Bank of America’s purchases of Countrywide and Merrill Lynch, and PNC’s purchase of National City. On a gross basis (prior to the reduction by the purchase accounting marks), Moody’s loss estimate is $633 billion, or 11.4% of loans outstanding at December 31, 2007. Essentially, we believe charge-offs equal to 1.7% of loans were eliminated through purchase accounting write-downs. Note that these estimates exclude securitized credit cards.

The charts and table below summarize our gross loss estimates in dollar and percentage terms by asset class for all rated U.S. banks (Figures 1 and 2). Each asset class is broken down as follows: charge-offs that have been eliminated through purchase accounting write-downs, 2008 charge-offs, 2009 charge-offs, and the remaining losses that would need to be incurred to reach our full estimate. Rated U.S. banks charged off $88 billion of loans in 2008 and $152 billion in 2009, leaving $296 billion, or 5.3% of loans, to be charged off in 2010 and 2011 to reach our full estimate. Therefore, rated U.S. banks have recognized 45% of our anticipated net charge-offs. On an asset class basis, we believe 42% of residential mortgage losses have been taken versus 30% for CRE.

And despite some minor good news in the trend, the overall pattern is still one which should force financial analysts to reevaluate their Strong Buy ratings on most banks:

Although the increase in charge-offs between 2008 and 2009 is substantial, the quarterly charge-off trend moderated at the end of 2009 with aggregate charge-offs actually declining slightly (from $41.3 billion to $40.2 billion) between the third and fourth quarters of 2009. This slow down in net charge-off recognition for rated U.S. banks did not change our forecast of the amount of charge-offs rated U.S. banks will incur, but it has changed our expectations regarding the timing of when these losses will be recognized. Previously, we had anticipated that rated U.S. banks would incur elevated charge-offs through 2010 and return to a more normalized level of charge-offs in 2011. However, we now anticipate that banks will still be grappling with elevated charge-offs through at least the first half of 2011.

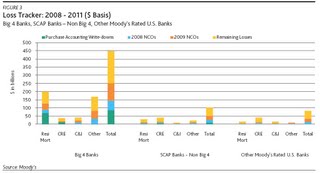

The TBTF Big 4 (BofA, Wells, JPM and Citi) comprise the bulk of the charge off risk. The Big have merely gotten Bigger, and now represent an even more concetrated threat to the US economy once true marks are let out of the bag.

Figure 3 summarizes our gross loss estimate in dollar terms for the following bank groups: “Big 4 Banks”, “SCAP Banks – Non Big ”, and “Other Moody’s Rated U.S. Banks” . Our gross loss estimates for the Big 4 Banks, SCAP Banks – Non Big 4, and Other Moody’s Rated U.S. Banks are $447 billion (12.9%), $104 billion (10.4%), and $81 billion (7.5%), respectively. In comparison to our estimate that rated U.S. banks are 45% of the way through their net charge-offs, we believe the Big 4 Banks are 46% of the way through their net charge-offs, while SCAP Banks – Non Big 4 and Other Moody’s Rated U.S. Banks are each 43%.

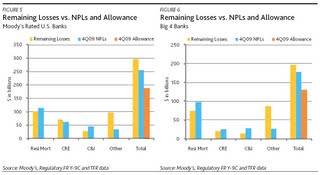

And here is how many remaining losses at all banks and the Big 4 will still need to be digested.

Full report here.

From the Moody's report:

Moody’s estimates that rated U.S. banks will incur $536 billion of loan losses between 2008 and 2011, equal to 9.7% of loans outstanding at December 31, 2007. We have incorporated this amount into our views of banks’ capital adequacy and into our ratings. This amount has been reduced for the purchase accounting marks taken on residential and commercial mortgage portfolios in recent acquisitions, including JP Morgan’s purchase of Washington Mutual, Wells Fargo’s purchase of Wachovia, Bank of America’s purchases of Countrywide and Merrill Lynch, and PNC’s purchase of National City. On a gross basis (prior to the reduction by the purchase accounting marks), Moody’s loss estimate is $633 billion, or 11.4% of loans outstanding at December 31, 2007. Essentially, we believe charge-offs equal to 1.7% of loans were eliminated through purchase accounting write-downs. Note that these estimates exclude securitized credit cards.

The charts and table below summarize our gross loss estimates in dollar and percentage terms by asset class for all rated U.S. banks (Figures 1 and 2). Each asset class is broken down as follows: charge-offs that have been eliminated through purchase accounting write-downs, 2008 charge-offs, 2009 charge-offs, and the remaining losses that would need to be incurred to reach our full estimate. Rated U.S. banks charged off $88 billion of loans in 2008 and $152 billion in 2009, leaving $296 billion, or 5.3% of loans, to be charged off in 2010 and 2011 to reach our full estimate. Therefore, rated U.S. banks have recognized 45% of our anticipated net charge-offs. On an asset class basis, we believe 42% of residential mortgage losses have been taken versus 30% for CRE.

And despite some minor good news in the trend, the overall pattern is still one which should force financial analysts to reevaluate their Strong Buy ratings on most banks:

Although the increase in charge-offs between 2008 and 2009 is substantial, the quarterly charge-off trend moderated at the end of 2009 with aggregate charge-offs actually declining slightly (from $41.3 billion to $40.2 billion) between the third and fourth quarters of 2009. This slow down in net charge-off recognition for rated U.S. banks did not change our forecast of the amount of charge-offs rated U.S. banks will incur, but it has changed our expectations regarding the timing of when these losses will be recognized. Previously, we had anticipated that rated U.S. banks would incur elevated charge-offs through 2010 and return to a more normalized level of charge-offs in 2011. However, we now anticipate that banks will still be grappling with elevated charge-offs through at least the first half of 2011.

The TBTF Big 4 (BofA, Wells, JPM and Citi) comprise the bulk of the charge off risk. The Big have merely gotten Bigger, and now represent an even more concetrated threat to the US economy once true marks are let out of the bag.

Figure 3 summarizes our gross loss estimate in dollar terms for the following bank groups: “Big 4 Banks”, “SCAP Banks – Non Big ”, and “Other Moody’s Rated U.S. Banks” . Our gross loss estimates for the Big 4 Banks, SCAP Banks – Non Big 4, and Other Moody’s Rated U.S. Banks are $447 billion (12.9%), $104 billion (10.4%), and $81 billion (7.5%), respectively. In comparison to our estimate that rated U.S. banks are 45% of the way through their net charge-offs, we believe the Big 4 Banks are 46% of the way through their net charge-offs, while SCAP Banks – Non Big 4 and Other Moody’s Rated U.S. Banks are each 43%.

And here is how many remaining losses at all banks and the Big 4 will still need to be digested.

Full report here.

posted by ENSO Advisors at

2:51 PM

![]()

<< Home